Use Cases¶

The General Unified World Model is designed for anyone who needs to reason about how the world works -- from hedge fund PMs to government analysts to AI agents. Each use case involves projecting to the relevant subset of fields, training on available data, and querying predictions.

Macro-Financial Risk Analysis¶

Who: Hedge fund PM, risk analyst, macro strategist

A hedge fund PM needs to understand recession risk, rate paths, and equity exposure given current macro conditions.

from general_unified_world_model import World, project

from general_unified_world_model.schema.business import Business

bound = project(

World(),

include=[

"financial", # yields, credit, FX, equities, crypto

"country_us.macro", # GDP, inflation, labor, housing

"regime", # growth/crisis/transition mode

"forecasts.macro", # recession probability

"forecasts.financial", # credit stress, rate path

],

entities={

"firm_AAPL": Business(),

"firm_NVDA": Business(),

"firm_JPM": Business(),

},

d_model=64,

)

graph TD

subgraph Observe

A["10Y Treasury: 4.25%"]

B["CPI YoY: 3.1%"]

C["Unemployment: 3.8%"]

D["VIX: 18.5"]

end

subgraph World Model

E["Financial Layer"]

F["Macro Layer"]

G["Regime Latent"]

end

subgraph Predict

H["Recession Prob 3M: 12%"]

I["Credit Stress: 0.35"]

J["Rate Path: cutting"]

K["AAPL Fair Value: ..."]

end

A --> E

B --> F

C --> F

D --> E

E --> G

F --> G

G --> H

G --> I

G --> J

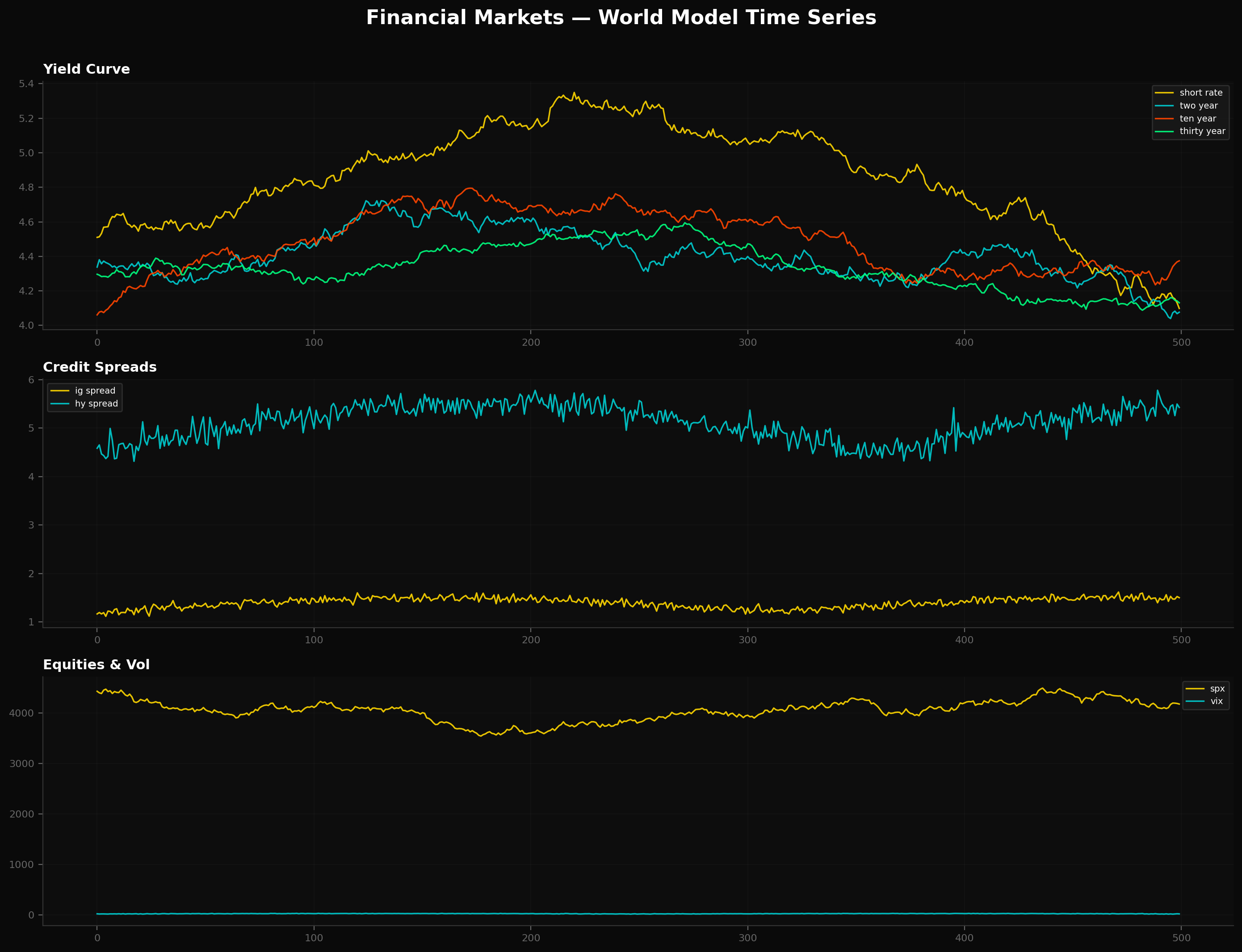

G --> KData sources: FRED (39 macro series), Yahoo Finance (equities, FX, commodities, crypto), earnings data for tracked firms.

What the model learns: How inflation expectations propagate through the yield curve. How labor market tightness affects Fed policy. How equity risk premia respond to credit conditions. All through shared latent structure -- no hand-coded rules.

Source: examples/05_train_financial.py

Geopolitical Risk & Commodity Exposure¶

Who: Commodities trader, geopolitical analyst, defense strategist

A commodities trader needs to understand how geopolitical tensions affect energy and metals prices.

from general_unified_world_model import World, project

from general_unified_world_model.schema.country import Country

bound = project(

World(),

include=[

"resources", # energy, metals, agriculture

"country_us.politics", # US policy stance

"country_cn.politics", # China policy stance

"events", # news and policy events

"regime", # global regime state

"forecasts.geopolitical", # conflict risk

],

entities={

"country_ru": Country(), # Russia

"country_sa": Country(), # Saudi Arabia

},

d_model=64,

)

Data sources: Yahoo Finance commodities (CL=F, NG=F, GC=F, SI=F, HG=F), ACLED/UCDP conflict data, GDELT news events.

What the model learns: How sanctions on Russia affect European natural gas. How OPEC+ decisions propagate to copper demand expectations. How conflict risk feeds into gold positioning.

Coming soon: live conflict prediction

Real-time geopolitical event prediction from news embeddings. The rotating globe will update with model predictions as events unfold.

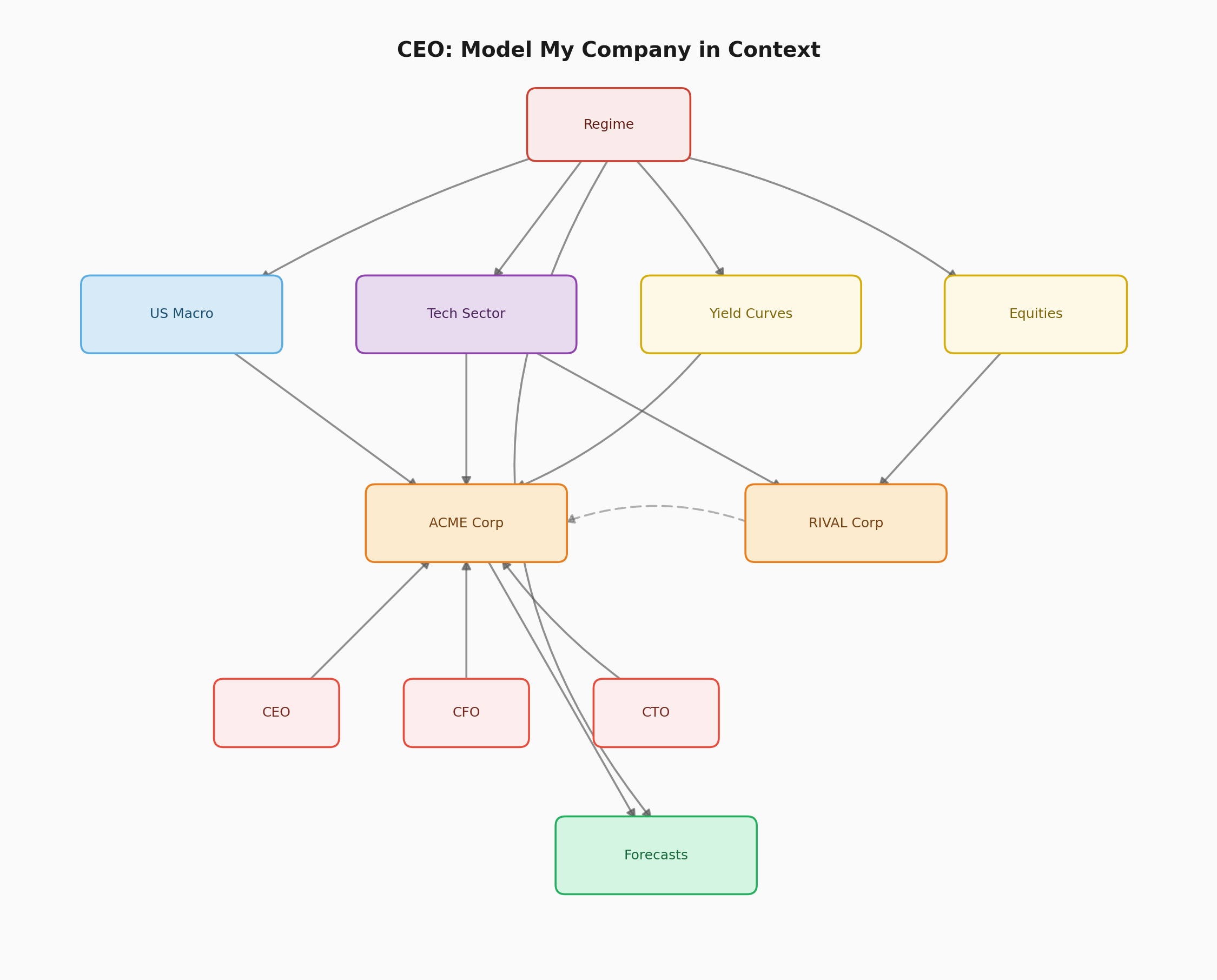

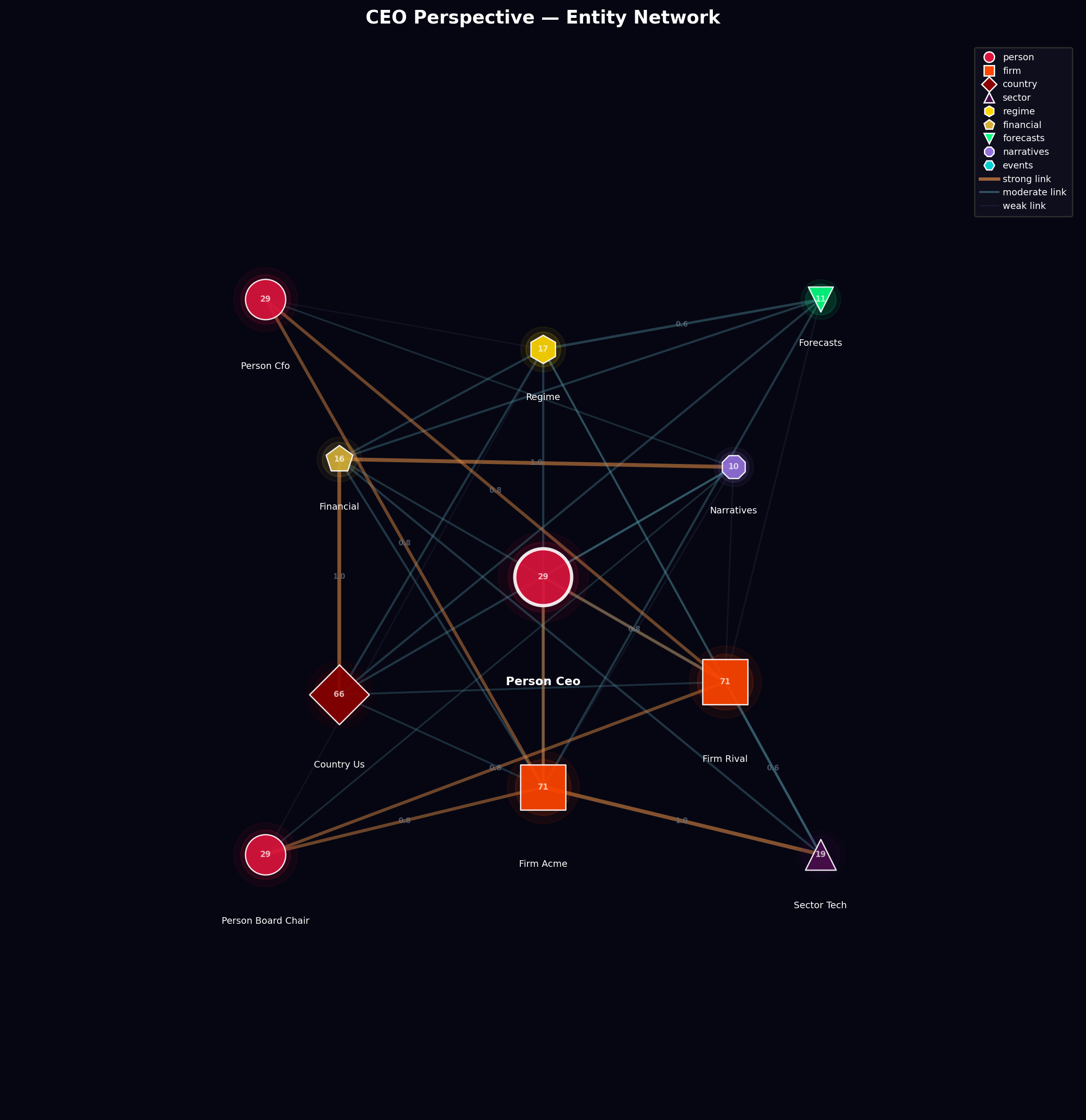

Corporate Strategy & Competitive Intelligence¶

Who: CEO, CFO, board advisor, strategy consultant

A CEO needs to understand how macro conditions and competitor moves affect their strategic position.

from general_unified_world_model import World, project

from general_unified_world_model.schema.business import Business

from general_unified_world_model.schema.individual import Individual

bound = project(

World(),

include=[

"financial.equities",

"country_us.macro",

"regime",

"forecasts.business",

"narratives.elites",

],

entities={

"firm_ACME": Business(),

"firm_RIVAL": Business(),

"person_ceo": Individual(),

"person_cfo": Individual(),

"person_board_chair": Individual(),

},

d_model=64,

)

Data sources: Yahoo Finance equity prices, quarterly earnings (revenue, margins, R&D spend), FRED macro context.

What the model learns: How macro conditions drive consumer spending (and therefore AAPL revenue). How NVDA's data center demand correlates with Fed policy (cheap money -> tech capex). How competitive dynamics between firms create correlated risks.

Source: examples/02_ceo_company_model.py

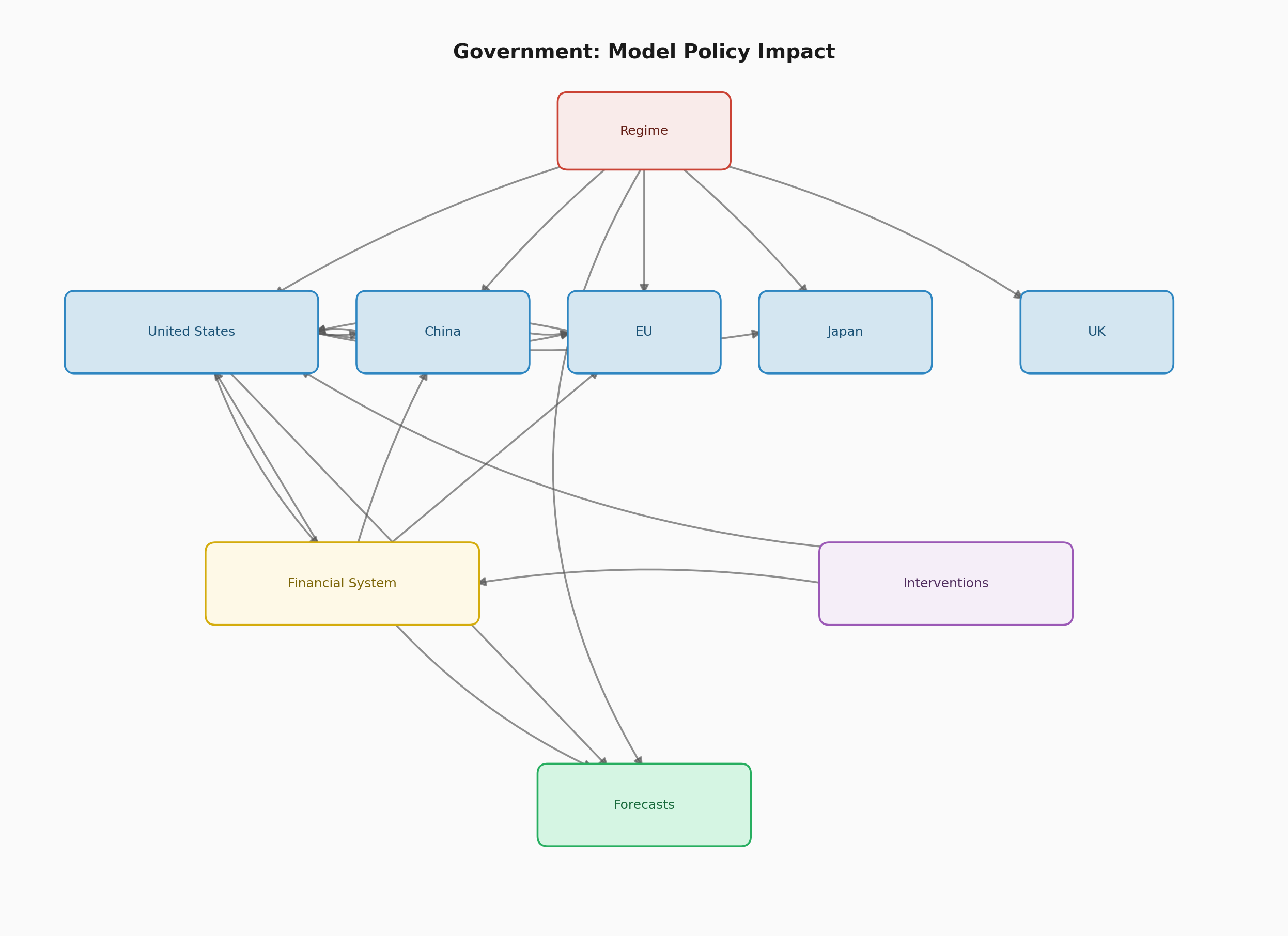

Government Policy Impact Analysis¶

Who: Central bank economist, Treasury analyst, policy advisor

A central bank economist needs to understand how monetary policy transmits through the economy.

from general_unified_world_model import World, project

from general_unified_world_model.schema.country import Country

bound = project(

World(),

include=[

"country_us", # full US: macro + politics

"financial", # markets respond to policy

"interventions", # monetary + fiscal tools

"regime",

"forecasts",

],

entities={

"country_cn_extra": Country(),

"country_eu_extra": Country(),

"country_jp": Country(),

"country_uk": Country(),

},

d_model=128,

)

graph LR

subgraph Policy Action

A["Fed Funds Rate: 5.25%"]

B["QT: $95B/month"]

C["Forward Guidance"]

end

subgraph Transmission

D["Yield Curve"]

E["Credit Conditions"]

F["Housing"]

G["Labor Market"]

end

subgraph Outcomes

H["GDP Growth"]

I["Inflation"]

J["Financial Stability"]

end

A --> D

A --> E

B --> D

C --> D

D --> F

E --> F

E --> G

F --> H

G --> H

G --> I

E --> JData sources: FRED (50+ series covering yields, credit, labor, housing, sentiment), IMF WEO forecasts, BIS cross-border statistics.

What the model learns: The full transmission mechanism from policy rate changes through the yield curve, credit conditions, housing, and labor markets to GDP and inflation outcomes. Cross-country spillovers from US monetary policy to emerging markets.

Source: examples/03_government_policy.py

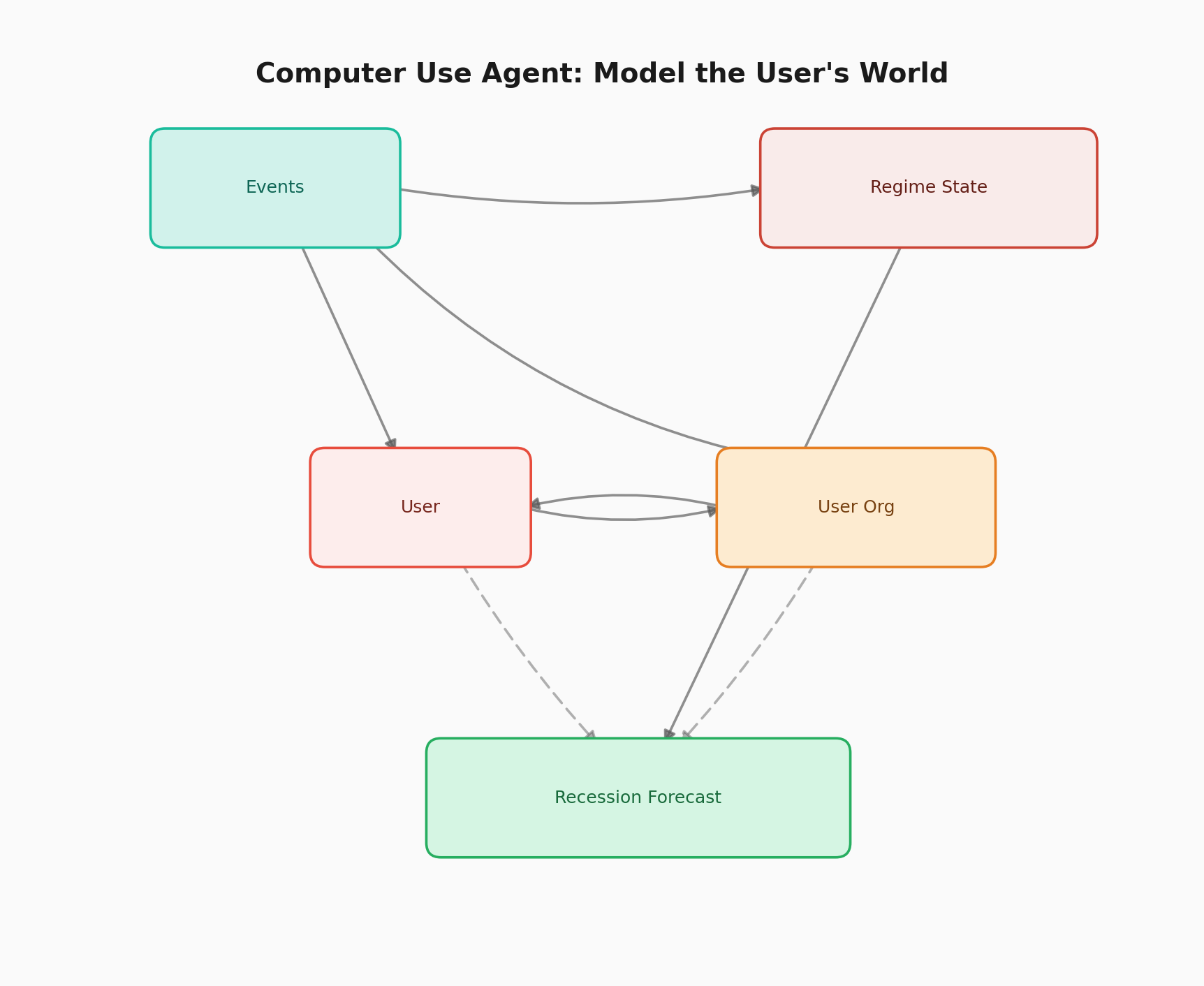

AI Agent World Context¶

Who: AI agent developers, autonomous system designers

An AI agent operating in the real world needs a compressed understanding of "what's happening" to make better decisions.

from general_unified_world_model import GeneralUnifiedWorldModel

model = GeneralUnifiedWorldModel(

include=[

"narratives", # what people are saying

"events", # what just happened

"regime", # world mode

"technology", # tech frontier

"forecasts", # where things are heading

],

d_model=64,

)

# The agent queries the world model as context

model.observe("events.news_embedding", latest_news_embedding)

context = model.predict()

# context["regime.growth_regime"] -> "expansion"

# context["forecasts.macro.recession_prob_3m"] -> 0.08

What the model provides: A structured, calibrated summary of world state that an agent can use for decision-making. Instead of raw news feeds, the agent gets a compressed latent that captures cross-domain dynamics.

Source: examples/04_computer_use_agent.py

Custom Dataset Integration¶

Any dataset can be integrated by declaring InputSpec and OutputSpec mappings:

from general_unified_world_model import DatasetSpec, InputSpec, OutputSpec

# Map your private data to world model fields

my_spec = DatasetSpec(

name="Internal Risk Model",

input_specs=[

InputSpec(

key="credit_score",

semantic_type="Corporate credit risk score",

field_path="financial.credit.ig_spread",

),

InputSpec(

key="revenue_forecast",

semantic_type="Quarterly revenue forecast",

field_path="firm_ACME.financials.revenue",

),

],

output_specs=[

OutputSpec(

key="default_prob",

semantic_type="Default probability",

field_path="forecasts.financial.credit_stress",

),

],

)

The LLM-powered annotator can also do this automatically:

from general_unified_world_model.llm.dataset_annotator import annotate_dataset

spec = annotate_dataset(

name="my_data",

columns=["revenue", "eps", "guidance", "sector"],

sample_values={"revenue": [42.5, 43.1, 44.8], "eps": [1.23, 1.31, 1.42]},

description="Quarterly earnings data for tech companies",

)

Source: examples/05_train_financial.py

More use cases coming soon¶

Planned examples

- Healthcare system modeling: Patient outcomes, hospital capacity, pharmaceutical pipeline

- Climate & energy transition: Renewable adoption, carbon pricing, grid reliability

- Supply chain resilience: Semiconductor supply, logistics bottleneck detection

- Election forecasting: Polling, economic indicators, social sentiment → electoral outcomes

- Pandemic early warning: Novel pathogen risk, healthcare capacity, travel restrictions